CENTRAL PARK TOWER MAKES IT A JANUARY TO REMEMBER

JANUARY 2023 NEW DEV CONDO MARKET UPDATE

Feburary 5, 2023

- Compared to the pre-pandemic 2015-2020 average, fewer deals were signed, but they were more expensive

- Compared to that same average, demand for $4M+ luxury units was 33% higher this January

- Manhattan and Brooklyn both recorded trophy contracts - $63.5M at Central Park Tower and $17.5M at Olympia Dumbo

- Queens was the only borough where demand was higher this January compared to the pre-pandemic January average

- Long Island City’s The Greene reported 15 contracts in January, although some may have been previously unreported

- Despite the $17.5M contract at Olympia Dumbo, demand for Brooklyn was anemic and missed its historical target for total dollar volume

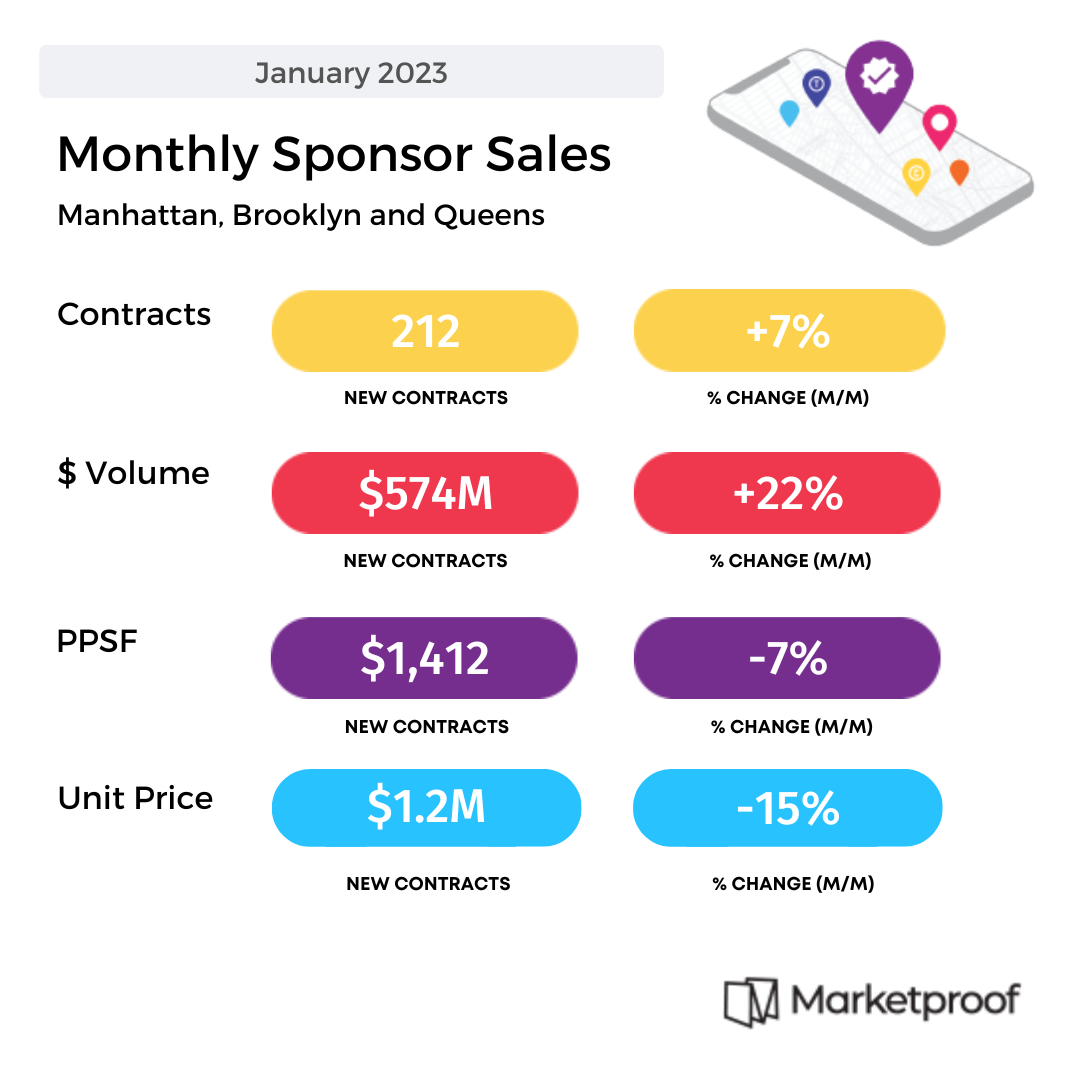

Although buyers were 10% less active this January than in years past with 212 contracts signed, recent deals were more expensive. Compared to the pre-pandemic benchmark, the median price increased 13% to $1,365,000 and the median PPSF rose 14% to $1,607.

The $63.5M contract at Central Park Tower was large enough to significantly move the total dollar volume needle from $483M to $574M.

“Compared to the pre-pandemic 2015-2020 average, it would have been an ordinary January had Extell not signed three units at Central Park Tower listed for a combined $90M. And, although mortgage rates are 50% higher than their average across that pre-pandemic period, demand is only 10% under par, so we believe the forecast looks favorable as the Fed begins to tap the brakes on further hikes.”

Kael Goodman - Co-Founder and CEO of Marketproof, Inc.

Luxury

January was a big month for the $4M+ luxury sector with all metrics higher. 32 contracts were signed, 33% more than the pre-pandemic benchmark and the $63.5M contract at Central Park Tower boosted total dollar volume from $196M to $327M. Median PPSF was up 8% to $2,798 and median price increased slightly to $6,737,500.

Of the 32 luxury deals this month, 30 were signed in Manhattan. Central Park Tower led the way in terms of both deal volume, 3, and total dollar volume, $90M. Besides the deal on residence #114 asking $63.5M, the building also recorded another big ticket contract for $19.3M and is now 45% sold. Four projects recorded two contracts, and One Waterline Square was the clear leader among them with a $27M contract on #PHA and now only a single unit stands between the developer and sellout.

Within our November report, we said that Olympia Dumbo defines the luxury market in Brooklyn, and never has that been more true than in January with a signed contract on Penthouse A asking $17.5M. Two Fifty Six North Ninth Street inked the other luxury deal in Brooklyn, a 4-bed listed at $4.295M, closing out the 10-unit building.

Manhattan

Thanks to the $63.5M contract, January’s total dollar volume, $433M, was 26% higher than its pre-pandemic 2015-2020 benchmark. However, that whale deal is muted within the median metrics - price, and PPSF - and they were much more on par with their benchmarks, at $1,990,000 (–5%) and $1,994 (+2%), respectively. Deal volume, too, was mainly at parity with its benchmark at 104 contracts signed (–2%).

Top Performers by Contract Volume

300 West 30th Street

300 West 30th Street was on the leaderboard for the past 3 weeks, so it’s not surprising that the building led Manhattan's new development sales during January with 10 contracts on 1- and 2-beds ranging from $1.095M to $1.735M. The building has been on the market for only 8 months, yet is nearly 20% sold. If the building's impressive sales velocity continues at its current pace, it will be sold out by this time next year. Aleksey Gavrilov and Joseph Grosso of Corcoran are handling sales.

450 Washington

450 Washington is on the leaderboard with 7 contracts, six of those for 2-beds ranging between $2.15M and $2.85M, and a 4-bed last asking $6.39M. The offering plan is now effective after only 2 months on the market. Sales and marketing for this waterfront, cooperative conversion are being handled by Corcoran Sunshine Marketing Group.

Manhattan Top 3s

Top Contracts

Central Park Tower #114 asking $63.5M

5-bed asking $9,478 PSFOne Waterline Square #PHA asking $27.0M

5-bed asking $4,112 PSFCentral Park Tower #95W asking $19.3M

3-bed asking $6,281 PSF

Top Closings

109 East 79th St #PH17 sold for $30.0M

5-bed closing at $4,576 PSF109 East 79th St #PH18 sold for $25.5M

3-bed closing at $3,944 PSFXoco 325 #8 sold for $17.2M

4-bed closing at $3,908 PSF

Brooklyn

The borough was similar to the city as a whole in that the deals signed this January, compared to years past, were more expensive but fewer. The median price was 13% higher at $995,000 and the median PPSF increased 8% to $1,231, but demand for Brooklyn's new development, measured by 71 contracts, was significantly lower than its pre-pandemic benchmark of 101. Relatively so few contracts were signed in fact that, even with the $17.5M deal on the penthouse at Olympia Dumbo, total dollar volume, $108M, was short of the historical average.

Top Performers by Contract Volume

111 Montgomery

111 Montgomery tops the leaderboard with 6 contracts signed on studio, 1-, 2-, and 3-bed units ranging from $525k to $1.8M. On the market for nearly 4-years, the project is now 77% sold and could sell out before year’s end if the current sales velocity continues. Tamara Abir, Jacqueline Gill, and Carrie McCue of Compass represent the developer.

Brooklyn Point

Brooklyn Point recorded 4 contracts in January on 1-, 2-, and 3-bed units ranging in price from $1.235M to $2.8M. On sale for nearly 5 years, the building has now sold over half of its inventory, an important milestone considering the size of the offering at 481 units. Serhant partnered with Extell Development in November 2020 to assist with sales and marketing.

Brooklyn Top 3s

Top Contracts

Olympia Dumbo #PHA asking $17.5M

4-bed asking $4,097 PSFTwo Fifty Six North Ninth Street #6B asking $4.3M

4-bed asking $1,745 PSF510 Driggs Avenue #2B asking $3.3M

3-bed asking $1,812 PSF

Top Closings

168 Plymouth #PHD sold for $5.0M

3-bed closing at $2,435 PSF510 Driggs Avenue #PHB sold for $2.6M

2-bed closing at $2,160 PSF98 Front Street #9B sold for $2.1M

3-bed closing at $1,419 PSF

Queens

Although demand for the borough was robust, total volume was too light relative to the other boroughs to prevent NYC’s numbers from sliding below their pre-pandemic average. Queens activity was the reverse of the city as a whole in that more deals were signed, 37 (+29%), but the median price was smaller, $795k (–16%). Still, total dollar volume increased 24% to $33.74M, as did median PPSF, up 23% to $1,424 which, interesting to note, is significantly higher than the median PPSF in Brooklyn.

Top Performers by Contract Volume

The Greene

The Greene reported 15 contracts in January, although some may have been previously unreported. The deals were a mix of studio, 1-, 2-, and 3-beds ranging from $510k to $2.275M. Although sales of this 129-unit condo tower launched less than 3 months ago, Michael Bethoney, Nayi Shen, Marina Kote, and Patrick Gorny of Nest Seekers International are only a single contract shy of declaring the offering plan effective at 15% sold.

The Georgian

The Georgian lands on the leaderboard with 4 contracts during the month: three 1-beds listed between $435k and $535k and a 2-bed asking $550k. Sales for this 65-unit condominium conversion are being handled by William Tabler of Keller Williams.

Queens Top 3s

Top Contracts

The Greene #PH4C asking $2.3M

3-bed asking $1,684 PSFSkyline Tower #5309 asking $1.8M

2-bed asking $1,834 PSF10-64 Jackson Ave #3A asking $1.6M

3-bed asking $1,175 PSF

Top Closings

Tangram House West #PH3B sold at $2.9M

3-bed closing at $1,463 PSFSkyline Tower #5411 sold at $2.7M

3-bed closing at $2,005 PSFGalerie #210 sold at $2.1M

3-bed closing at $1,445 PSF

Report Methodology

- The average of January numbers during the period 2015-2020 is used as a normalized benchmark for comparison as it is the most recent period unaffected by the COVID pandemic.

- Report is based on reported contracts and may not represent all contracts signed

- Prices are based on the last asking price before a unit was put into contract

- New development contracts are sponsor stage (sponsor controlled) projects that are eligible to sell units

- Data as of 2/1/2023

Access available new development inventory, past sales for 250K condos, and pipeline of future projects.